Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv The Willis Report FOX Business September 3, 2012 6:00pm-7:00pm EDT

6:00 pm

gerri: tonight a very special edition of "the willis report" celebrating your financial independence. the road to prosperity can be no doubt him pay, and the show's purpose to guide you along the way. covering every angle of your financial life from where you should invest into choosing the best college for your kids and grandkids to getting an idea of how to launch a small business. it is never too late. the biggest financial decisions you ever need to make your in yr lifetime answered here tonight. welcome to type special edition of "the willis report."

6:01 pm

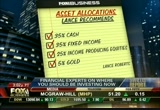

hello, everybody, i'm gerri willis. i don't know about you but i cannot shake that uneasy feeling about the economy and as a result translating into the markets high market volatility in recent months becoming the new normal for starting off the show with a simple question, where should you be investing now? to answer that, the panel of financial experts and advisors, lance robert. jamie foxx managing partner, and managing director of wealth held financial. where should i be invested in right now? speak of is a time, very challenging. this marketplace asset allegations sound like there is redundant but you have a balance in your portfolio amongst ducks

6:02 pm

and bonds and when i talk about that i think for most people looking for a little more yield, have to be focusing a dividend stocks and within bonds looking at yielding bonds like high yield bonds, convertible bonds and floating rate bonds. people think about bonds and think treasuries. gerri: is all about asset allocation? >> i think so. i think it is about the particular goals you have for your investment 65 you invest differently than 25 so investors put together a portfolio that take into consideration the time horizon. an allocation much higher in stocks or equities rather than the person retired would want an allocation not 100% equities. cheryl: 35% cash, 35% fixed income, some gold in there. tell me more about your ideas

6:03 pm

are asset allocation. >> mine is a little bit more simple. having diversified portfolio. the difference we add to it is we actually manage the risk of the market overall. we have been getting our clients out of equities in march and early april and into more cash and fixed income for the summer months as we see weakness in both the economy, domestically and internationally. last year we did exactly the same thing and increased allocations back to equities in october as the markets turned around and we got funding from the fed. by managing the risk of the market, we can reduce the drawdown so don't spend so much time trying to make up lost principle. >> it is not unlike an advisor to have tactical shifting to making calls when they get in, the summer months are slow, that is market timing and i don't feel you will get it right all

6:04 pm

the time at all. >> have gotten pretty much every call right, we are not market timers, we just reduce it. it is the same thing as playing poker. you don't bet on every hand with all your chips, that is how you run out of money. i'm moderating the risk of the market at any time in the market is declining, while i want to invest in equity risk when i can pick up return from fixed income where money is going into? gerri: there are people who don't only not only believe asset allocation, but they want to be all in cash, what do you tell those people tonight? >> if you want guaranteed negative returns, cash is a fantastic investment i don't think the average investor understands what cash means. they think it is safe and predictable and if interest rates are six or 7% is a fantastic place to invest but you should be using the cash to buy equities and gives her

6:05 pm

diversify. you have to think about purchasing power. you make investments in stocks have to think about the dollar i am investing today purchase more in the future. if it isn't, you shouldn't invest. gerri: you are talking about treasury bonds before. why should anybody buy treasuries right now? >> we would have said it is a bubble, i don't think you can market the chart, but if you look at other assets you can invest in to get some yield i would shy away from treasuries. that is guaranteeing you lost precision power over time the fed try to keep inflation. >> we are going to 1% on the 10-year, 2% on the 30-year period was 30% return just by buying treasuries over the next couple of years.

6:06 pm

we're in a deflationary economy that will be with us the next 10 to 15 years. you will be in real trouble long long-term. >> your guaranteeing yourself 1% return over 10 years. if you are buying next year or two coming to be worried about yield on on treasury but for 10 years you're making a call the next 10 years is great 1% greater return. gerri: i love it when people disagree on investing advice because usually there is so much ludicrous agreement on these things. i have to ask you about gold, do you like it? >> actually do like it for a portion of the portfolio but a lot of things people get a little bit overzealous buying too much of it. so my caution to all investors, everything in moderation. gold is a place of value, an interesting dynamic. gerri aren't people trading it like a stock now?

6:07 pm

isn't that done? >> i don't think so. people look at it as a safety play. i think gold absolutely have a place in the portfolio. >> the reality is you might be better off with gold mining stocks at least in that case we can look at the financials of the companies, but has not been as much of a correlation between golgoldmine stocks and gold, moe and more people are trading the etf as a momentum play and you cannot value something like that. gerri: last word. >> i agree do not want to own physical gold. you will not be able to get out of it in time that owning gold is a fear factor for this idea it is a safety trade, it has been a good non-corollary tha t. gerri: up next, back after the break and they will be disagreeing some more. that is why like about it.

6:08 pm

advice for people of all ages, plus now the time to sell your house, buy one, refinance? stay with us, we will answer your money questions, what you need to know.

6:09 pm

you see us, at the start of the day. on the company phone list that's a few names longer. you see us bank on busier highways. on once empty fields. everyday you see all the ways all of us at us bank are helping grow our economy. lending more so companies and communities can expand, grow stronger and get back to work. everyday you see all of us serving you, around the country, around the corner.

6:10 pm

us bank. has oats that can help lower cholesterol? and it tastes good? sure does! wow. it's the honey, it makes it taste so... well, would you look at the time... what's the rush? be happy. be healthy. less expensive option than a traditional lawyer? at legalzoom you get personalized services for your family and your business that's 100% guaranteed. so go to legalzoom.com today for personalized, affordable legal protection.

6:11 pm

gerri: welcome back to our special edition of "the willis report." our panel of financial experts are back focusing on your retirement questions including the best plan for you. welcome back all, i want to start to rock or not to rock. we had a tweet from somebody who said they are concerned, their son had gotten a job trying to decide where to invest, what do you say?

6:12 pm

>> depends if he is working for a company with a 401(k) plan i recommend he started their first and maximize and catch the match from the company. if he is talking about an ira versus a roth, iraq will probably be okay at a very young age. my one concern in general is there will come a time when the government starts looking for more tax revenue and a very easy place to go get more revenue is to reverse the tax free and of the ross. there may be an issue down the road for changes. gerri: i completely agree with you and i think it's a big danger for investors of all sorts. weigh in on this. is it possible? all kinds of tax-free investing for college planning purposes, is it possible washington might strip this away? >> anything is possible. i would hope of something that happened he would have a grandfathering, i think that is a little hopeful that it would be going forward and future

6:13 pm

contributions. that is a fear a lot of my clients have, rather the text doesn't say and uncertainty in the future. gerri: it is all about taxes when you're saving for retirement that seems to be something critical. key to really planning well, what do you say, how do you protect yourself from high taxes? speak i think you to maximize your 401(k) contributions. put money away from if you know for ephedra getting earnings will not be assessed tax. but you have to tax distributions because different income sources have different tax treatments. capital gains is taxed another way, so when you pay attention you have to make sure that you taxed test every decision you make or else you will give away money at a time interest rates are so low, tax rates of 15% it is a bad combination.

6:14 pm

>> talk a lot about allocations, but where do you put certain asset classes but it is tax-deferred account or not because the things that will grow quickly in a higher tax rate should be in your nontaxable account. you want them outside the ira or the 401(k). the location plays a part in looking to retire, maybe run away. gerri: what you say of taxes and retirement? >> i agree with everything both gentleman just said. particularly if you're planning for retirement don't forget breakfast don't set aside completely whole life insurance. whole life insurance creates income into the insurance products and the withdrawals are tax-free later in life and come out as loans and will not be affected much by any kind of tax law changes that might occur part of an estate planning process. part of an estate planning

6:15 pm

process trying to hedge off some of your future estate tax issues a whole lot of interest, tax tax-free income down the road. gerri the one thing i think everybody asks or a question i hear over and over again, how much it might saving for, how much, what is my number? >> i think it replace the income you aryou're living off of now. lots of retirees and people i manage money for think they can live off of less, you cannot plan that way, have you plan living and what you have been living on now in retirement and if you don't your lifestyle will change dramatically. that may not be a reality for everyone. gerri: i'm already paying for my lifestyle right now. if i can pay double, i would, but i am not doing that, so how can i save enough for retirement? speaker that is the whole basis of financial planning to looking at this throughout your earning

6:16 pm

capacity and think about what kind of lifestyle and run numbers. it is different depending on where they lived with their spending habits is. is not the answer you want to hear. gerri: what is my savings goal? >> is never enough. there are three points to all of this i think need to be added. planning for financial retirement don't use a stagnant rate of return. a lot of mistakes are banking on 7% per year and if i have that money, don't go for that. look at the last 12. the other thing is very quickly a recent study showed retirees on average live on 95% of what they were making during their working years and multiple going to retirement thinking they will live on 80. don't forget the majority of the health care costs will come towards the end of your life. >> many require more in

6:17 pm

requiremenretirement because the enjoying more, they are doing more. gerri: we are going to have to wrap it for now, coming back to answer more of your questions later in the show. up next the look of a state of small business and what you need to know if you're going to launch your own thriving small business with very little capital, we will talk about that, don't go away. away.

6:19 pm

gerri: the best way to raise capital without putting your own money on the line, if it's possible? or small-business expert says yes. that is next.

6:21 pm

gerri: welcome back to our special edition of "the willis report." look, if you're considering their own small business, my next guest says there are three important questions to ask yourself. i want to start with this idea, i'm not starting a business down because the economy is so bad but look at this, burger king, fedex, microsoft started in a recession, now is not a bad time. >> i don't think you never time the market. if there is a strength, there is a weakness and vice versa. there is also really good things you can get out of your business. you can get better deals with vendors, better payment terms, so never try to time the market, i always save you a really good customer opportunity and you're the best person to serve that opportunity, that is when you start a business. the first question you want to

6:22 pm

ask yourself is is this something i should do? lots of people go forward with a risk isn't worth the reward. far too many owners who work too many hours for the same or less pay with more stress than when they had their own job. they have to go through the business planning process. so may start a business because they are passionate and have a great idea, they don't look at the hard facts. is this enough of the opportunity to be worth it for me? gerri: what about the risk? >> this is something you will be putting in your time and effort. i always say there is a rule of three, taking three times as much, three times as difficult as you anticipate.

6:23 pm

gerri: they're always telling if i had to do it over again, i would not but i'm glad i did. can i test drive my ideas? >> this is the most important thing you should do is test it out before you invest your time and money and effort, there are simple ways you can do this. before you quit your job, tested out on nights and weekends. when the passion goes away, so why did i get myself into it? thank you there is a way to dofy it on a small scale. try a food truck with a lower investment. if your retailer said of opening up a big space with huge overhead, try a pop up shop. gerri: what if i don't have a lot of capital?

6:24 pm

they want their own business. >> most people don't have a lot of capital going into your own business. if you don't have the capital yourself, you have to go out and unfortunately venture capitalists only fund a fourth of the business. a creative way to do that is with crowd of funding like kick starter.com, go to your network and say i have a really cool business idea or a project or product, will you sponsor me? another reason is to raise capital but you can do it in a different way from kick starter to come up with incentives to say you are coming up with a product for $50 i will send you the product when it is done, but i will put your name on the box for $1000 you can pick what color the box is. gerri: a lot of people just call mom or dad. hope they will make the money.

6:25 pm

>> mom and dad don't have the money anymore. but if they do, be very careful because you are layering a professional relationship on top of a personal one. you have to assume they will lose the entire investment so they cannot afford to lose it. gerri: i think that is great advice, i know everybody is looking at it. up next, housing questions answered. are you following me online? if not, what are you waiting for?i w tweet me and follow me on facebook, we love to hear from f you. we asked over 3,000 doctors to review 5-hour energy

6:28 pm

and what they said is amazing. over 73 percent who reviewed 5-hour energy said they would recommend a low calorie energy supplement to their healthy patients who use energy supplements. seventy-three percent. 5-hour energy has four calories and it's used over nine million times a week. is 5-hour energy right for you? ask your doctor. we already asked 3,000.

6:29 pm

gerri: home prices on the right to little bit, so is the housing crisis over or soon to be over? my next guest has moved more than $7 billion of real estate. joining me now, vice chairman. always great to see you. you know, the problem in real estate when you interview people is they often kind of skates the truth, but you are always a straight shooter, how are we doing in the market, are we headed for a recovery now? >> attribut we are treading neae bottom. going up a little bit is always good. but it's all terrific. now fix all the other issues, employment issues, structural issues. until that is resolved i don't see a recovery in the cards. gerri: so you really think we need a recovery before we see real recovery in the housing. so in that income committee on

6:30 pm

home already, would she be doing? >> refinance your mortgage. if you have a mortgage chances are the rates are better now than when you took it out even if you took i about five months ago. i refinanced my mortgage for the seventh time and interes an interest-rate i cannot believe it's is better than the last one. everybody should look into refinancing their mortgages even if they're unde they are underws are trying to work with you to see if fannie and freddie were put in a program that might let them also refinanced their mortgages. gerri: far from being in the way, lots of questioned bankers saying they're not doing what they can to help people out there. >> i've seen banks being very helpful. they're trying the best they can to get everybody on the right track so the whole country gets on the right track.

6:31 pm

gerri: on a lot of people want to upgrade because their family got bigger. what is your recommendation about sinking more money into a house might have bought at the top of the market? >> if you're doing it very cautiously, counting their pennies and really planning it, say it is probably okay to redo the kitchen, the floor, make them darker and lighter and do bathrooms. i would be very careful, judicious and generic. don't do a black kitchen. gerri: not everybody wants that. >> do something generic and it will make it much more marketable. gerri: people have to be careful about the money they're putting into their home because you do not know if you're going to get return if you pay top dollar. >> if you are judicious and generic you will be okay. gerri: what is my house really

6:32 pm

worth? hire an appraiser, how can you decide what that umber should actually be? so you're deciding to sell and will put your house on the market in the next few months. >> : a few local realtors, ask for a writ opinion of value. documenting the opinion of the value with comparable sales and giving it to you to review. three broke is coming, you will get three different numbers, it is shocking to me. if you're looking at it as a homeowner with interest at heart, you can discern between them and find out what your home is really worth. gerri: your advice to homeowners right now who has been a hard road. very difficult for a lot of people. if you're underweigh underwatert should you be doing? >> if you need to get out, look into renting your property.

6:33 pm

it hasn't been stronger in a very long time, maybe you can rent your home, rent your apartment and downsize. and the people who had a four bedroom house, they don't need a four bedroom home. they pocket the difference and they can laugh, all about kicking the can, thing that everybody is doing. as long as you can survive it, you'll be okay. gerri: the second home, the vacation home not just first homes underwater, it is also vacation homes. isn't this a big opportunity for people who have been looking for that to retire or vacation? >> to be a great time because interest rates have not been lower in forever. prices in general also have not been lower since early 2000. it is a great time, but the judicious and careful and bid

6:34 pm

aggressively and weight. hold back. gerri: so difficult in the housing market because you get so excited about that property. >> they cannot know what you're thinking, you have to pause. gerri: i have no poker face. dolly lenz, thank you for coming on. now maybe the time to buy your home if you happen to have millions of dollars burning a hole in your pocket. we have a few options in the top five most expensive homes for sale in the u.s. in santa barbara, california, $84 million to get more than 2000 acres including a private beach, a lagoon, macadamia nut tree. everybody wants one of those not to mention 14 guesthouses. number four, new york city. $90 million you can be the eight story former home of lucille roberts. number three, the beverly house

6:35 pm

in beverly hills, california. featuring a nightclub, tennis club, and a hand carved wood paneled library. you can rent a mansion for 600 grand per month. and number two, in manhattan, $150 million gets you an apartment at 11,000 square foot apartment with floor to ceiling windows overlooking central park. the number one most expensive homes for sale in the u.s. is in los angeles, 35,000 square feet of paradise can be yours for the low price of $125 million. i guess 12 bedrooms, 15 bathroom mansion with 200 person ballroom is worth it? i don't know. make sure your money is where your heart is. plus, paying for college loan has become a full-time job these days with record high tuition costs but is it worth it? our financial panel is back next.

6:36 pm

money? our financial panel is back. [ owner ] i need to expand to meet the needs of my growing business. but how am i going to fund it? and i have to find a way to manage my cash flow better. [ female announcer ] our wells fargo bankers are here to listen, offer guidance and provide you with options tailored to your business. we've loaned more money to small businesses than any other bank for ten years running.

6:39 pm

why? i thought jill was your soul mate. no, no it's her dad. the general's your soul mate? dude what? no, no, no. he's, he's on my back about providing for his little girl. hey don't worry. e-trade's got a killer investing dashboard. everything is on one page, your investments, quotes, research... it's like the buffet last night. whatever helps you understand man. i'm watching you. oh yeah? well i'm watching you, watching him. [ male announcer ] try the e-trade 360 investing dashboard. gerri: talk about your sticker shock on average cost for public college jumped 15% over the last four years. and how do you begin paying for it?

6:40 pm

managing partner of harris financial group and managing director of well: financial planning. my favorite question, i will start with you, what do you do, save for retirement, or do you save for college or your kid? >> save for retirement, very easy to ask this question because you have to think about the long-term ramifications. parents say they are obligated to pay for school, i paid my own way through school. it can be done, there are ways to do it but if you think of yourself paying for schools, the end of the day you'll become a burden on your children and that is not the legacy you want to leave your kids. gerri: it is a happy balance. 20 of cultural aspects of this where people feel they are obligated and you have to respect that.

6:41 pm

also look at grants and scholarships taken consideration the fact and circumstances. gerri: the numbers are lower. how do you choose the best college? speak up has taught me the economics lesson when i went to school so you can go anywhere you want but you have to pay for. with a good economic lesson for me and i got tempted at a lot of schools, i came out with no loans, but the important thing is not to disregard education. if you look at the unemployment rate among college graduates, i think it is important people value education and don't disregard it because it will cost money, huge investment you can do when you are young and pay dividends forever. gerri: the story i hear over and over again is people getting journalism degrees and they will

6:42 pm

go to work and they will make 25,000 in that first job, they're not at all prepared of what they will be making. >> look, most people whatever degree they get in college unless it is a specific degree like engineering very rarely work in the field they got their degree in. life tends to take in a variety of situations. get a degree you can always get a job with, counting, financing, engineering, and you can always get a job but you can always work on your passion later. it will open doors for you. speaker don't discount the state schools because you have to look at what kind of industry you may be going into, what is your major an look to wonderful state schools well known in journalism for instance and you get a great education. gerri: a lot of them went to safe schools, not just about what school you go to.

6:43 pm

sometimes it is not what the child brings to the program. i want to talk about vehicles for savings now. we thought these were great vehicle for a long time, now people have major questions, what is your point of view? >> when they were originally designed, they were designed to be a buy and hold strategy. it works in a bull market like in the 80s and 90s. we will not see that for many, many years ahead because of our debt issue so the fundamental flaw is you only change them once per year. it potentially can hurt you and the returns have been exceptionally low, people better off in cash. >> have to disagree. if you're going to sit in cash for long-term, that is a loser. if the tax benefit and have programs that change the allocation overtime, you are

6:44 pm

less and less risk oriented and you also could take the allocation in your own hands, i have done this for a number of claims and pay the allocation and make it what we want it to be, not the actual 529. gerri at the end of the day she and the kid take the onus, the burden of the savings on themselves and work and what they value that education a lot more if they are involved in paying for it? >> of course. if you do not give a child and incentive to have a good job, what are they going to do? play for four years? you have to be careful what you are recommending 100 person because each state has its own plan, so they're desperate. it is kind of hard to know which one is good and which one isn't you have to do a lot of research to make sure you get it right. they are seven, four, two.

6:45 pm

i made contributions to a certain time and i stopped because i want the value of money to take over so it is a bi-hold strategy for younger children. gerri: is really about starting early if you're going to put some money down. don't go away, hold that thought, we're coming back with some really interesting stuff if you're headed down the altar anytime soon. are you planning in addition to the family? we have got you covered next.

6:46 pm

you see us, at the start of the day. on the company phone list that's a few names longer. you see us bank on busier highways. on once empty fields. everyday you see all the ways all of us at us bank are helping grow our economy. lending more so companies and communities can expand, grow stronger and get back to work. everyday you see all of us serving you, around the country, around the corner. us bank. gerri: a new report shows parents will spend a quarter of a million dollars for one kid for 18 years before college. advice for mom and dad in two minutes.

6:49 pm

gerri: $25,000 the average price of a car or a down payment on a home or even the average cost for a semester in college. these days it can be the average cost for a wedding. of course it could be far more than that. back with me now, we were talking in the break about this. you said people who spent 25,000 for a bar mitzvah. >> i know people paying 40 to 50,000 for a bar mitzvah. i think the problem is people think about the immediate time, not disciplined about their future going back to last segment about college planning. start early and forecast down. what is the cost for my retirement in the future? what is that compounding 40,000, 50,000 you are paying. gerri: i wanted to talk about marriage and getting divorced.

6:50 pm

a lot of people don't even think about the financial consequenc consequences. they are huge. speakers eliminate joint property state very bad cutting your assets and half including a 401(k) plan and honestly divorce from a moral basis should be your very last option. it is a function it is a financial disaster for people because generally what you are seeing right now so i serve it out yesterday, the divorce rate for baby boomers has risen by 20% in the last five years. these people are very late age heading into early retirement now getting divorced losing half their assets, now what do you do for retirement? gerri: not just mom and dad, it is their children. what do you tell people who come and say we're thinking about

6:51 pm

getting a divorce, how is that going to impact them? what do you say? >> counseling is much cheaper. we try to tell them basically the same thing the other guest has told them, but we say pushing the reset button, you basically believe everything you have done up to this point, push the reset button and start all over again unless you are extremely wealthy it is usually a budget buster and retirement buster for a lot of people. gerri: and an emotional buster seven and back in so many ways if there is a way to avoid it, you really should. the other end of the location, it sounds so not romantic for me. >> i think a prenup makes sense in certain circumstance. at the end of the day you agree to agree to no different than a partnership in the business aspect and a tough conversation to have.

6:52 pm

when you get married you need to have that conversation potentially other conversations about credit history, budgeting, what your makeup is in the way you spend money versus your partner and also have old people involved in the process because the worst thing is when one person does everything, the other is oblivious and that creates a problem, i think. gerri: do you go along with a prenup? >> i agree with everything because a marriage is a partnership just like going into business with somebody. good documentation, good conversations build good fences and it creates the open expectation that i know what i'm getting into. the biggest two reasons for divorce our finances and sex. many people, the reason they are not having sex is their finances are not in good shape. find out what you're getting into and to use a prenup or not, but having some kind of agreement you sit down and work through the process of creating

6:53 pm

an overall relationship much healthier in the long term. gerri: if people knew how much debt their partners had before they went to the altar, that would be such a great first step to having a happy marriage. let's go on to planning for kids. what kind of planning in ready to have children financially. speak to determine whether or not you know what you're going to do for childcare. if you have both people working, how are you going to afford to let one person stay home, are you going to pay for expensive day care? you have to decide on those things right up front. budget for things like paper, food, clothing, you do not have any idea how much they cost. when you're looking to have children, most people don't plan on having children. they find out after the fact. you have private education and

6:54 pm

things like that, the money adds up and heads up but i would like to say the thing i see among young parents, they want their kids to do everything. have them in five sports, they cannot afford it, they don't understand the kid needs something to look forward to or else they will be bored. you cannot expect them to have anything later on. would i field telling her parents, to be mindful of the fact that children need to have a few things to do, that where they can learn what they like as opposed to doing ballet, piano, they are not good at any of it. speaker that goes back to the same conversation about getting married that only your finances but what do you expect from your family and with respect to the lifeguard t-- lifestyle to provr family. can you afford it, does your hosting have to change?

6:55 pm

in some cases people suddenly move. that becomes a financial burden as well. these are the type of things that have to be discussed, communication is key and forecasting what kind of lifestyle you want for you, your marriage and children is really important. gerri: last word, go right ahe ahead. >> as a father for i will tell you this, if you're ever thinking about having children, go babysit somebody's kid for the weekend and it will guarantee to change your life. gerri: we cannot end on that note. >> i love every one of them to death. they are a huge responsibility financially, emotionally, it changes everything. if you like going out on the weekend and having a nice weekend at a nice restaurant, that will be over. gerri: and there will be returns later on. >> absolutely. gerri: we really appreciate your

6:57 pm

questions. when you're caring for a loved one with alzheimer's, not a day goes by that you don't have them. questions about treatment

6:58 pm

where to go for extra help, how to live better with the disease. so many questions, where do you start? alzheimers.gov. the answers start here.

6:59 pm

gerri: and finally, if there's one thing we learned over the last hour, it is that you can control your financial destiny. it takes planning, determinati determination, but you can manage your money. i know it sounds easy but it is so important for all of us to set our financial goals and stick with it. tonight we are learned there are opportunities out there, you just have to know where to look and hopefully do able to show you a few. we cannot rely on the government to manage our money, we know that. who knows if social security will be around for decades to come. trust your instincts, you know what is best for you and your family. u

98 Views

IN COLLECTIONS

FOX Business Television Archive

Television Archive  Television Archive News Search Service

Television Archive News Search Service

Uploaded by TV Archive on